Measured Memo Q4-24

Hello Measured Investors,

Welcome to The Measured Memo – a concise note that shares our perspective on private investing and income-producing assets. We aim to make this the most value-packed investing email of your quarter…let’s go!

Market

The cross-current of news in today’s market can make for a confusing narrative. On one hand, we’ve beaten inflation, rates are on their way down and the stock market continues it’s bull run. Meanwhile, we’ve got tight credit, depressed asset prices and reports showing increasingly ‘hard times’ for many Americans.

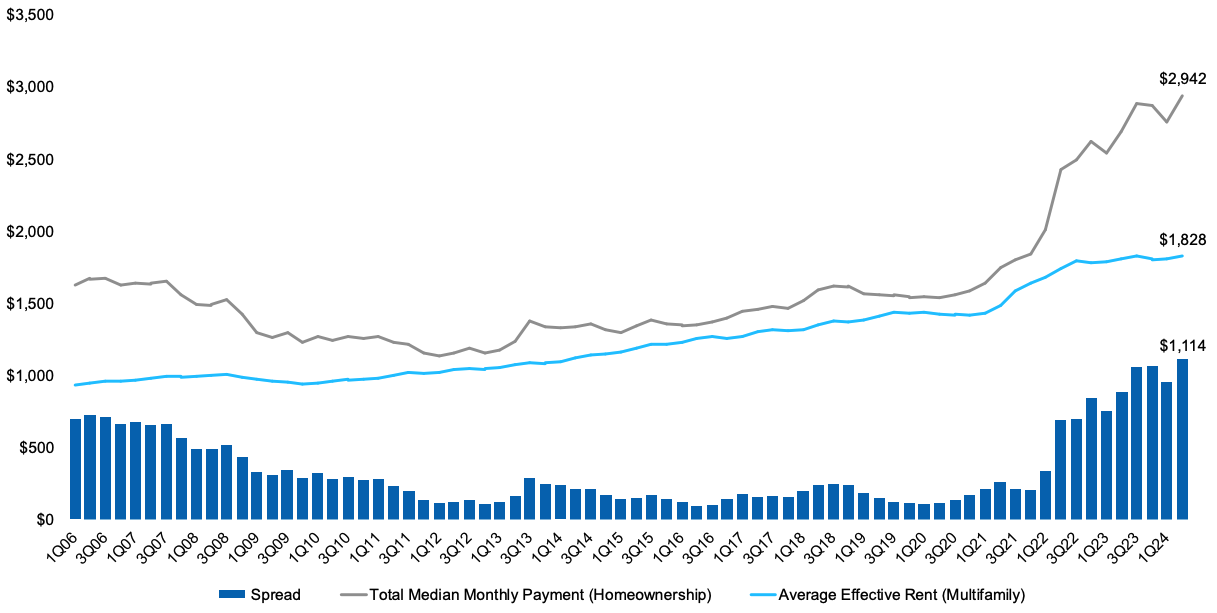

One topic that is always in the crossfires of this debate is housing. Here–the trend has been consistent for decades: it continues to get more and more expensive, in relative terms, to own a home. In fact, we’ve hit a new all-time high in the rent vs own ratio.

From Newmark’s Q2 Capital Markets Report: “Increasing 26.7% year over year, the spread between homeownership and rental costs grew to $1,114 per month in the second quarter of 2024.” The chart below visualizes the difference and emphasizes the fundamental need for affordable rental housing for much of the population.

As prices for single family homes continue to climb, we’ve seen the opposite move for multifamily properties. In many markets the cost-per-door of an apartment has decreased 20-30% from the peak. This is a direct result of the dramatic increase in interest rates; and is exactly what the Fed intended when it raised rates–to deter speculation on leveraged assets.

In 2020 to 2022, when credit was unsustainably cheap, there was hubris in the multifamily market and many buyers overpaid for assets. They were confident someone else would come along and buy the property for more, even though many of these acquisitions made no sense from an operational or cash-flow perspective. These buyers missed on two fundamental tenants of long-term asset investing: (1) reasonable leverage and (2) positive cash flows.

As we documented last time, the market is now loaded with deals that were purchased with too much debt and not enough cash flow. These are problematic situations for all involved. We’ve seen this trouble brewing first-hand by reviewing the financials and touring the grounds of many properties that collect less in rent than they pay in interest.

The big question now is–how does the market rid itself of all this troubled debt?

Strategy

History teaches us that most likely outcome will be a quiet and “behind the scenes” transfer of wealth as each ‘bad’ deal is worked out one-by-one with owner, lender and an opportunistic buyer. In the absence of a total crisis like 2008 (which of course is still possible), the market will be forced to ‘write down’ these assets to a level that attracts a new buyer.

The lenders that funded the bad deals will take a hit, the current owner will have equity wiped out and this procession will continue until the last “over-paid” apartment is washed from the system.

This transfer has already started. The most knowledge and capable buyers have begun to pour capital into discounted multifamily assets. Blackstone, the private equity giant, made news when it closed on a portfolio of apartments this year for $10 billion.

This purchase was notable, but the back-story is even more telling. Blackstone had been actively trying to purchase these exact properties for a decade, but could not get a deal done. In April, the owner was forced to sell–at a 35% discount to previous valuations.

Today, we find ourselves with a long list of target properties that we would love to own and operate, if only the price to acquire them would come down to our desired number. This has been our focus and will continue to be. We currently have multiple offers out on properties with varying levels of distress. Patience is required as we wait for the cost basis that supports low-risk, high-impact, fundamental investing.

Portfolio

The Measured Capital portfolio remains unchanged in terms of property count which has enabled a focus on operations and asset management of active deals.

In seven of nine assets, we are effectively done with value-add construction and occupancy is stabilized above 90%. One thing that we’ve learned over the past quarter–now is not the time to try to aggressively push rents and risk turnover. Instead, we’ve put a priority on happy residents and earning renewals by providing a superior experience and value.

With this strategy, we are able to keep our rent rolls full–crucial in these times of uncertainty. A good example is our newest asset in Jacksonville–our team is now signing renewal leases with residents a full 6 months before their current lease expires. This has the effect of locking in 18+ months of revenue, in addition to reduced maintenance and turn costs. Renewal rates are averaging over 10% increase there. In Des Moines, we are offering renewals with 14 and 18 month terms; having similar affect.

To us, this seems like the obvious and right thing to do. It’s contrary to market norms and does require patience, but results have increased our conviction in this operating style. We believe its the foundation that will enable future properties to succeed and we are aggressively seeking assets that fit into this business plan.

References

- Newmark Q2-24 US Capital Market Report (link)

- Apollo 2024 US Housing Outlook (link)

- Deep Dive: Private real estate’s surprise problem child (link)

Thanks for reading. At Measured Capital, we are committed to always putting ourselves in the place of highest potential – which for us, often means connecting with like-minded investors like you.

Please forward this note to any trusted friend you feel could benefit as well. We welcome your feedback and are grateful for your trust.