Measured Memo Q2-24

Hello Measured Investors,

Welcome to the Measured Memo – a concise note that shares our perspective on private investing and commercial real estate. We aim to make this the most value-packed real estate email of your quarter…let’s go!

Market

We spent 2 days in January attending this year’s NMHC (National Multifamily Housing Conference) – it’s the biggest and most attended industry event of the year. Besides providing high-quality face time with all major brokers in our focus markets, a conference like this also provides a great “feel” for the industry. As expected, there was cautious optimism in the air – these CBRE metrics give a good pulse.

Many of the professionals attending were feeling beat-up after 2023. If you live on commissions from the selling or financing of an asset and that asset class’s transactions go down 61% year-over-year, that is going to hurt! But brighter days are ahead. Every major broker we met with reported being “slammed with seller proposals and BOV requests” – the two activities that lead to future sales.

And yes – interest rates continue to be main challenge and driver of sentiment in the space. In the news, there is a lot of talk about how higher rates make for higher debt service payments and the obvious pain that causes. But many in the media miss the other slice of that knife…the reduced loan amounts. Higher debt payments mean you get less debt proceeds on the same property, forcing investors to bring more cash to every deal.

Which brings us to the “elephant in the room” topic of the private investing space – the ridiculous amount of dry powder on the sidelines waiting to be deployed, reported at over $2.5T (yes, trillion). Some of this cash is very patient (family offices with strict underwriting) and some is not patient (REITs and institutions who must deploy some capital by way of their business model).

Here’s our take regarding the multifamily space – there will be discounts and distressed sales, but we simply don’t see a tsunami of foreclosed deals or extended markdowns because there is so much capital actively looking for such opportunities. Every time there is distressed asset on the block, multiple funds rush in to capitalize on it, which creates a floor on pricing.

Strategy

One of the core values of Measured Capital is a commitment to the long-term. Our faith in the multifamily asset class is based on a 25+ year view of markets, population and economics. Additionally, our careers and networks are chock full of examples extolling the value of commitment to a long-term perspective.

Let’s also recognize that someone saying they are long-term and actually acting long-term are very different. This dynamic is being tested hard right now given the uncertain future of interest rates over the next 12 months. Let us make two statements on that, one bold prediction and then a caveat to walk it back:

- The next move in the interest rate cycle is down; rates will be lower in the near future.

- We have no idea when or how fast that move in rates will be; but it will likely be faster than expected.

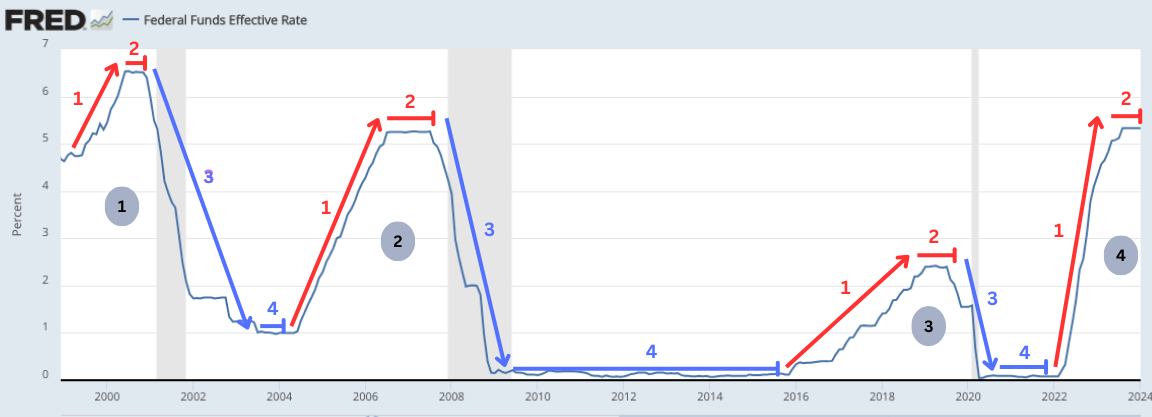

These statements are formed purely via observation of history. This dance is nothing new. The United States has been doing it since the founding of the Federal Reserve Bank in 1913. Here is a chart of targeted Fed Funds interest rate over the past 25 years. We are currently in stage two of the 4th cycle as described below.

First, fiscal policy gets restrictive (1) to control the speed and quality of credit issuance. Then things get tight in the economy so rates plateau (2) as policy makers “wait and see.” It becomes clear policy is too tight and rates drop quickly (3) to get more credit into the market. Eventually, everyone is satisfied for a period where things plateau again (4), until we start to over-lend and the cycle starts once more.

No predictions, just observation and response – stage 3 is next. And since we can't time it, we’ll stick with fixed rate debt, positive leverage and long-term holds, thank you very much.

Portfolio

Since our last update, we’ve been fortunate to secure two fantastic assets that line up perfectly to the thesis.

First, DSM4 and Harbach Lofts in Des Moines, IA. This is a 103 unit Class-A building that includes retail space and is unique in that we were able to secure 10 years of interest-only debt. Measured investors contributed $4M in equity to this project and now own one of the best located apartments in the MSA. We closed on Dec 11th; you can see this property up close at harbachlofts.com.

Next, JAX1 and Hidden Oaks in Jacksonville, FL. This is a 64 unit community and an off-market deal that is nearly 2 years in the making. The property was build in 1989 and is being purchased at a very low cost basis. Measured investors will contribute $3.5M in equity to this project. Importantly, we just added $150k in additional LP equity which is available now. Please email me if interested.

Finally, as mentioned last year, we are “staying close to the rim” on a number of deals that we’d be happy to own at the right price. There will be multiple trips to Des Moines and Jacksonville by yours truly as we optimize our current assets and deal pipeline. We are forecasting 3 to 5 acquisitions this calendar year.

Thanks for reading; we hope this note brings you insight and confidence as you navigate the investing world and seek quality returns on capital. Please forward this note to any trusted friend you feel could benefit as well. We welcome your feedback and are grateful for your trust.