Measured Memo Q1-26

Published on:

March 23, 2026

Author:

Dan Reilly

Hello Measured Investors,

Welcome to the Memo, a concise note that shares our perspective on private investing and income-producing assets. We aim to make this the most value-packed investing read of your quarter. Let’s go!

Market

One of the hottest topics in the economy right now is inflation: the rising cost of housing, of energy, of food, of everything. It has become a massive part of the political debate and will likely influence elections for years to come.

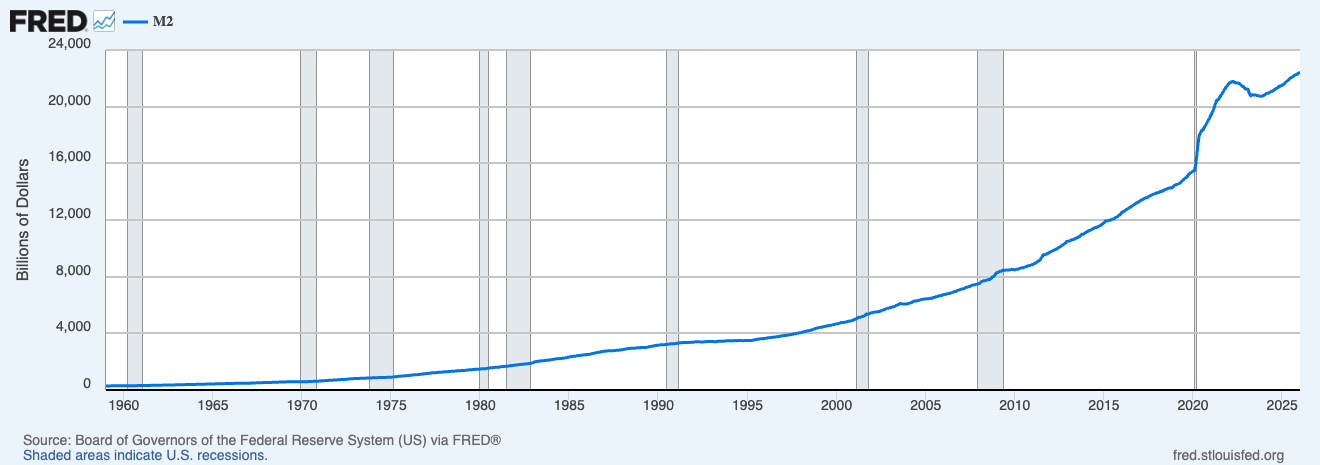

Of course, rising prices are nothing new. In fact, they are inherent to our economic system. Since 1913, when the Federal Reserve was established, the supply of currency in circulation has been growing consistently. This is by design. A growing economy requires a growing money supply, but it is a delicate balancing act.

The Fed's stated goal is 2 percent inflation per year. Sometimes they fall short and the economy sputters. Other times (looking at you 2021) they allow it to run much hotter and we all feel the personal pain of high inflation. I bring this up not to spur more political debate, but to point out how profoundly it shapes the case for hard assets and long-term investing.

The chart above shows the growth of the money supply (M2) in the U.S, and it clearly visualizes this story. When you buy a hard asset, you do so in today's dollars. The rents it generates and the price you eventually sell it for will be denominated in tomorrow's dollars, when more currency is in circulation. The same concept applies for financing; debt is borrowed in today's dollars and paid back with tomorrow's. This price expansion, compounded over decades, is the nominal growth that is built into hard assets.

Ray Dalio has done extensive research on more than 500 years of economic history to understand this pattern. His conclusion was remarkably consistent: in the later stages of a long-term debt cycle, which is where we find ourselves today, hard assets always rise relative to financial ones.

Which raises a simple question for every investor:

Do you want to own dollars, or do you want to own things priced in dollars?

Strategy

Clearly, your friends at Measured Capital reside in the "things priced in dollars" camp. So the next question becomes: what thing do you want to own?

For us, the answer stays consistent. Multifamily housing is, in our view, among the best investment vehicles available for long-term capital preservation and growth. This is because its fundamental qualities are uniquely suited to an inflationary environment.

Start with the demand. People need a place to live regardless of what the Fed does, who wins an election, or what the stock market does on any given Tuesday. That baseline demand produces recurring monthly income from an essential service. Layer on the ability to finance with long-term debt, drive performance through operational excellence and benefit from tax efficiency that few asset classes can match, and the structural case speaks for itself.

Short-term cycles will always deal their blows. The last three years are proof of that. Valuations compressed, credit tightened, and operators were humbled. But those cycles do not change what multifamily is at its core: an essential service, a physical asset, and a long-term store of value priced in tomorrow's dollars.

What they do change is the entry point. Commercial real estate values are still 20 to 30 percent off their peak. Credit is loosening. Sentiment is improving. The question posed above, do you want to own dollars or things priced in dollars, has the same answer it always did. The difference today is that the price of admission is lower than it has been in years.

Portfolio

Across our portfolio, performance over the past several months has improved meaningfully relative to the prior year. Operational momentum is strengthening, even where rents are under pressure.

In Des Moines, we have assumed full control of asset management and transitioned all properties to new management partners. In Jacksonville, strategic changes to onsite teams and operating processes are producing lower maintenance costs and improved resident engagement.

Workforce-oriented assets are still sensitive to affordability pressures, and concessions are sometimes required to maintain occupancy. What we can control is execution, and that is where our focus remains.

Looking ahead, we expect to be both buyers and sellers in 2026. Several assets are approaching the end of their stated business plans. While peak-cycle projections are unlikely to be realized, our low cost bases and conservative capital structures provide flexibility. Improving sentiment, expanding credit availability, and the prospect of rent growth should support successful exits that protect investor principal and recycle capital into the next opportunity.

We have been building toward this part of the cycle since we started. Conservative leverage, disciplined acquisitions, and hands-on asset management were not always fashionable during the boom years, but they are exactly the qualities that matter when markets stabilize. We intend to approach this next phase with the same discipline while loading up on quality assets that will benefit from the nominal growth inherent to our economic system.

References

- Multifamily At An Inflection Point – John Burns Research takes stock of where multifamily stands heading into 2026, covering how disciplined execution, policy risk, and value-add strategies are reshaping the apartment and build-to-rent markets at a key inflection point.

- IRR 2026 Annual Market Cycle Chart – Integra Realty Resources maps where 60+ major U.S. markets sit in the real estate cycle across every major asset class (multifamily is on page 2), and the picture confirms what we have been saying: most markets are now in recovery or early expansion.

- Takeaways from NMHC: Who Wants a Loan? – Jay Parsons reports from the industry's largest annual gathering that lenders are aggressively pursuing multifamily borrowers, debt capital is abundantly available at increasingly attractive terms, and the asset class remains the preferred collateral of institutional capital.

Best,

Dan & Greg